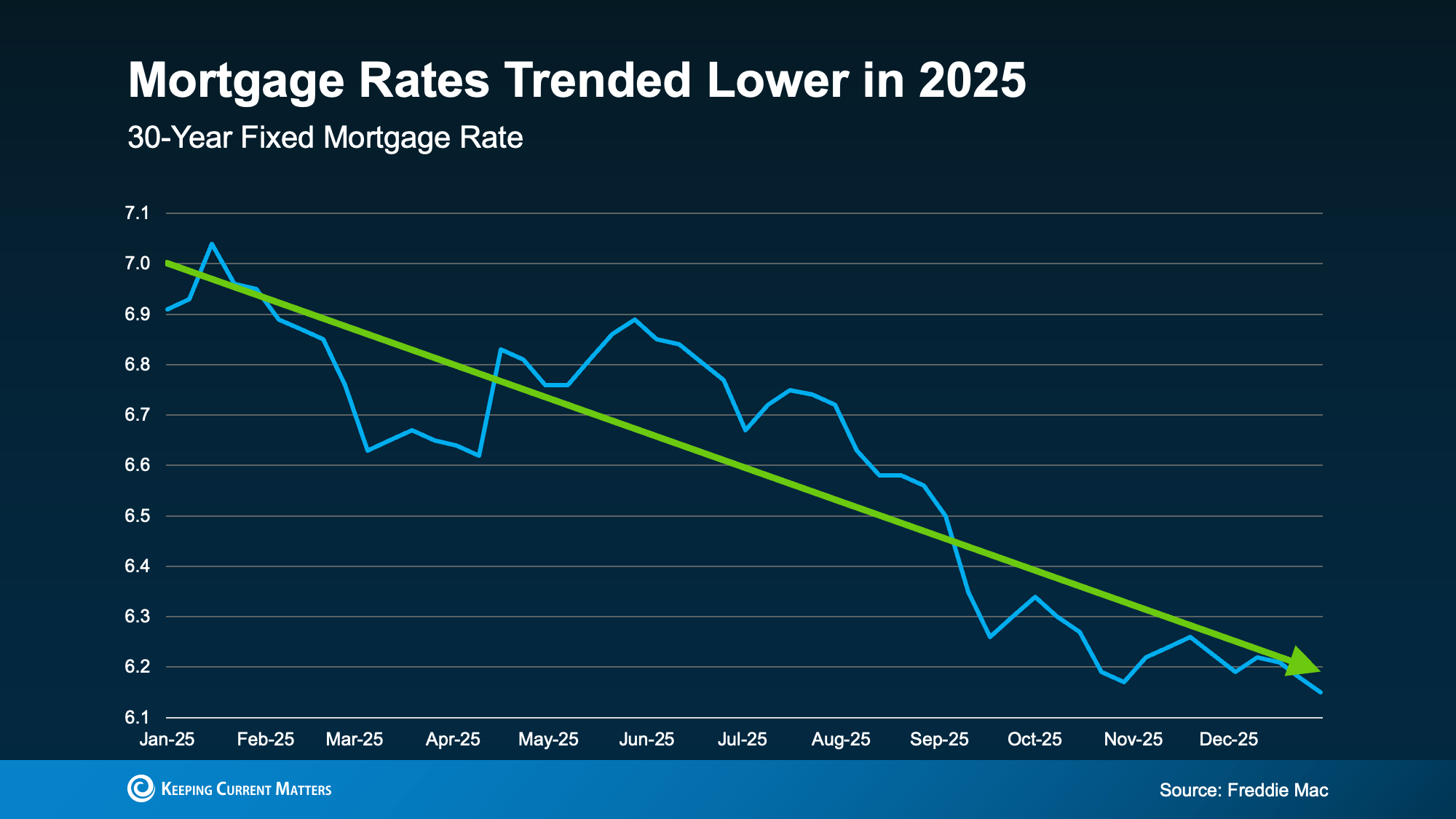

Affordability. It's the most talked-about issue in real estate right now, and understanding what impacts it can transform how you approach homeownership in 2025. The market has already delivered encouraging news: mortgage rates have dropped significantly from their 2023 peak near 8%, with recent activity pushing rates to the low 6% range and brief dips below 6%.

This isn't speculation anymore—it's happening. Recent Federal Reserve activity, including Fannie Mae and Freddie Mac purchasing $200 billion in mortgage-backed securities, has brought rates down to levels that are creating real affordability improvements. On a $500,000 loan, the difference between January 2024's 7.26% rate and today's rates around 6% represents approximately $400 in monthly savings. That's a meaningful shift that's making homeownership more accessible.

The Bigger Affordability Picture

Here's what many buyers don't realize: we're experiencing one of the strongest real estate markets beneath the surface in our lifetime. While headlines focus on challenges, the fundamentals tell a different story. Two-thirds of Americans either own their homes outright or have at least 50% equity. Inventory has been steadily improving throughout 2024 and into 2025, giving buyers more choices than they've had in the past five years.

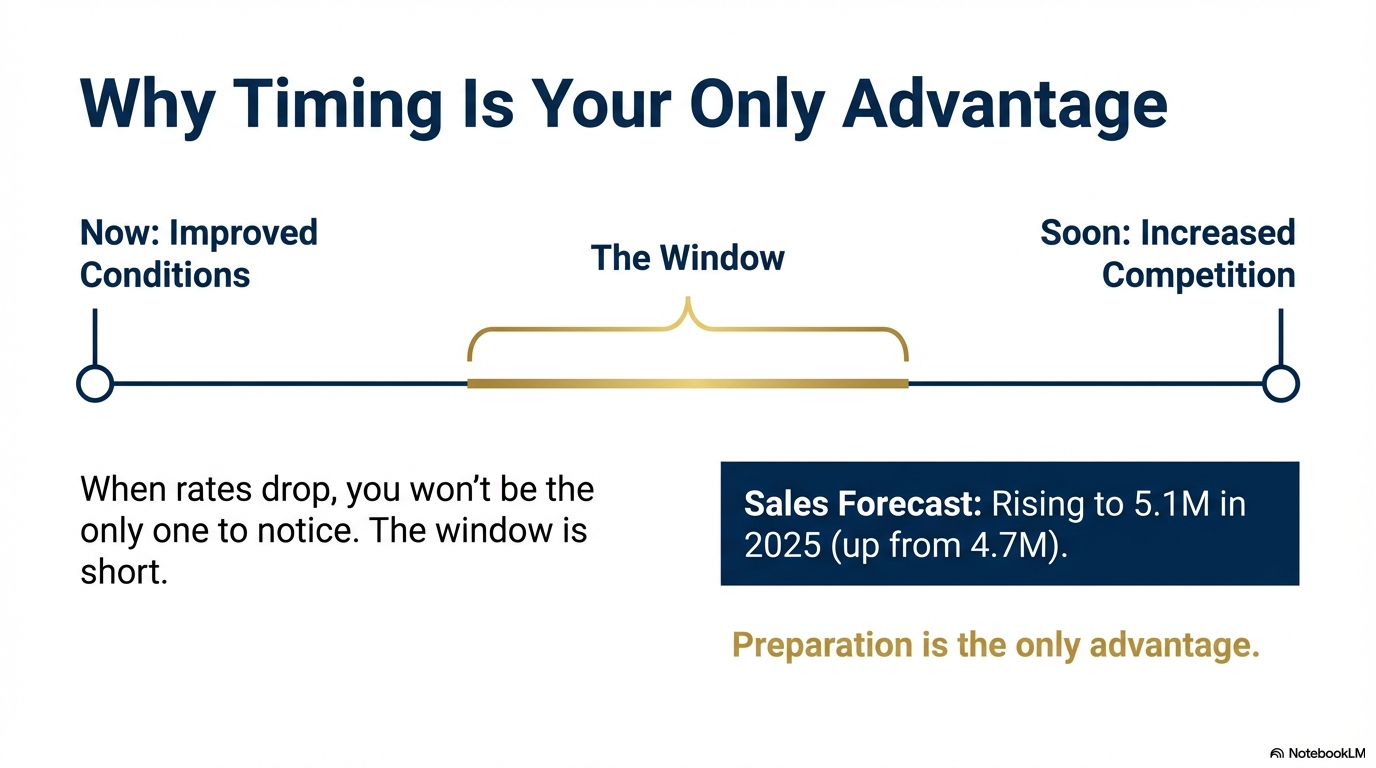

The convergence of declining rates, improving inventory, and wage growth outpacing home price appreciation creates opportunities for prepared buyers. But here's the critical insight: when rates drop and affordability improves, you won't be the only one who notices. The window between improved conditions and increased competition can be surprisingly short.

Understanding the Current Market Dynamics

The Federal Reserve's monetary policy shifts have started influencing mortgage rates in a favorable direction. While the Fed doesn't directly control mortgage rates, their decisions on the federal funds rate significantly impact the overall lending environment. The recent rate cuts signal a continued trend toward more affordable borrowing costs, with forecasts suggesting rates will hover in the low 6% range throughout 2025, with periodic dips into the high 5% range.

Why This Moment Matters

Politicians across the spectrum recognized housing affordability as the dominant issue in recent elections. This bipartisan focus means policy efforts are aligned toward helping more people achieve homeownership. Whether through mortgage rate support, inventory solutions, or addressing insurance and tax challenges, the spotlight on housing affordability creates a supportive environment for buyers.

Several factors are contributing to the current rate environment:

- Economic stabilization after post-pandemic volatility

- Improved inflation metrics approaching the Fed's 2% target

- Strategic employment market considerations

- Federal Reserve actions supporting mortgage market liquidity

Portland Metro Market Impact and Current Opportunities

On the national level inventory remains lean in the Northeast and Midwest, keeping those markets relatively tight with steady price growth.

Meanwhile in the South and West -- market conditions are different. The chart below shows the traditional seasonal peak and valley cycle in Portland Metro and clearly shows the trend is a slow but steady increase in the number of homes coming on market.

This creates a "steadier but not off to the races" market—healthier conditions without the frenzy of previous years. For buyers, this means:

- Enhanced affordability metrics

- More time to make informed decisions

- Less extreme competition than pandemic-era markets

- Competitive dynamics shifting in favor of prepared buyers

Strategic Preparation Steps

1. Financial Documentation Readiness

Organize your financial portfolio now to move quickly when rates drop further or the perfect property appears:

- Recent pay stubs and W-2s

- Complete tax returns (especially crucial for self-employed individuals)

- Current asset statements

- Documentation of any additional properties or investments

- Updated insurance information

The faster you can provide documentation, the faster you can lock in favorable rates when they appear.

2. Credit Profile Optimization

Your credit standing significantly influences your ability to secure favorable rates:

- Review your credit report for accuracy

- Address any discrepancies or issues promptly

- Maintain consistent payment histories

- Keep credit utilization ratios low

- Avoid opening new credit lines during the preparation period

3. Budget Analysis and Planning

Understanding your financial capacity is crucial in the current environment:

- Apply the 28/36% rule for mortgage qualification (monthly payment shouldn't exceed 28% of income; total debt should stay under 36%)

- Calculate potential monthly payments at various rate points

- Factor in additional homeownership costs (insurance, taxes, maintenance)

- Build reserves for closing costs and down payment

- Consider that wage growth is currently outpacing home price growth—a reversal from recent years

The monthly payment to buy a typical home is expected to drop below 30% of median income for the first time since 2022, improving the affordability equation.

4. Professional Pre-Approval Strategy

Strengthen your market position with proper pre-approval:

- Obtain a comprehensive pre-approval letter that shows sellers you're serious

- Consider specialized programs that help you compete effectively

- Understand the 60-90 day validity period of pre-approvals

- Prepare for quick renewal if necessary

- Be ready to lock rates when they hit favorable levels (like recent dips to 5.99%)

Timing Your Market Entry

While exact timing remains challenging, several indicators can guide your decision:

- Monitor Federal Reserve meeting schedules and announcements

- Track weekly mortgage rate trends—we're currently seeing volatility that creates opportunities

- Assess local market inventory levels in your specific area

- Consider seasonal market patterns

- Be prepared to act quickly when rates dip into favorable ranges

The lesson from market experts: even the forecasters don't know exactly what tomorrow brings. Rates can shift based on economic data, Fed actions, or broader market conditions. The key is being prepared to act when conditions align with your goals.

What Makes This Different

Here's the reality many buyers don't understand: home sales in 2024 and 2025 will go down as two of the slowest years in real estate when adjusted for population growth. Yet the market fundamentals remain strong. This isn't a market in distress—it's a market in transition to healthier, more sustainable conditions.

Current forecasts show:

- National home price appreciation of 1-2% (modest and sustainable)

- Rising incomes outpacing inflation, giving buyers more purchasing power

- Inventory continuing to increase through at least mid-2025

- Total home sales expected to rise by approximately 8% in 2025

Long-term Market Considerations

Understanding the bigger picture helps you make better decisions:

- Current housing inventory remains approximately 1.5 million units below historical averages

- Price appreciation may vary significantly by region—understanding your local market is critical

- Wage growth outpacing home price growth creates improving affordability over time

- Competition could intensify in desirable markets as rates improve further

Action Steps for Success

- Begin organizing financial documentation immediately

- Establish relationships with qualified local lenders who understand current programs

- Monitor market conditions and rate trends—but don't wait for perfection

- Prepare for quick action when rates reach your target or the right home appears

- Maintain flexibility in your housing criteria while staying focused on your core needs

Moving Forward with Confidence

The current market presents unique opportunities for prepared buyers. Rates have already improved significantly, inventory continues growing, and affordability metrics are moving in the right direction. Success requires preparation, market awareness, and strategic positioning.

Remember: the clients and buyers in your market are hearing national news daily, but they need local expertise to understand what it means for them. The difference between January 2024 and today represents real savings and real opportunity. Those who prepare now will be positioned to act when their moment arrives.

If something changes tomorrow, you'll adjust. That's the job. But right now, the fundamentals support taking action for buyers who are ready. Get your finances organized, obtain pre-approval, understand your local market, and be prepared to move when conditions align with your goals.

This is a steadier market, built on stronger fundamentals than we've seen in years. That's exactly the environment where prepared, informed buyers succeed.